42 duration of a coupon bond

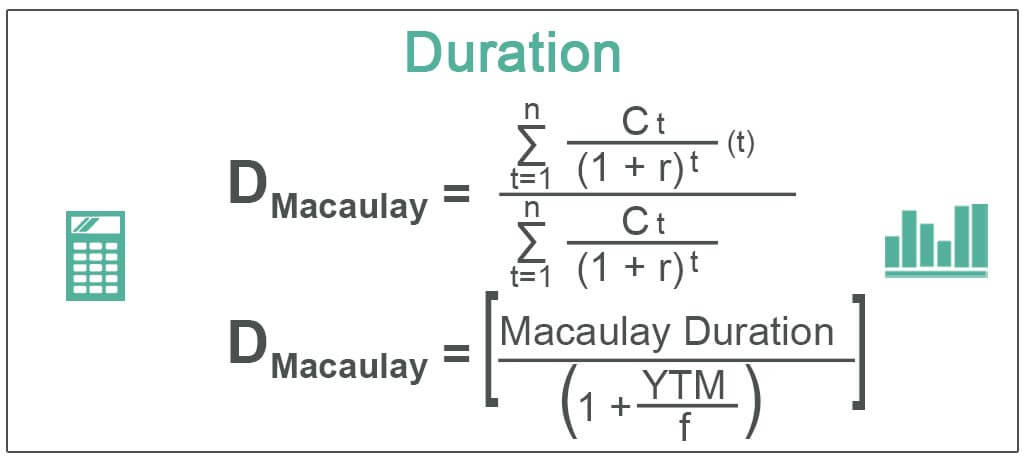

What Is the Macaulay Duration? - Investopedia Sep 29, 2022 · Macaulay Duration: The Macaulay duration is the weighted average term to maturity of the cash flows from a bond. The weight of each cash flow is determined by dividing the present value of the ... How to Calculate the Bond Duration (example included) Jul 23, 2022 · FV = Bond face value; C = Coupon rate; t i = Time in years associated with each coupon payment; Once you calculated the Macaulay duration, you can then apply the following formula to get the Modified Duration (ModD): MacD ModD = (1+YTM/m) Example of calculating the bond duration. Imagine that you have a bond, where the:

Coupon Definition - Investopedia Apr 02, 2020 · Coupon: The annual interest rate paid on a bond, expressed as a percentage of the face value.

Duration of a coupon bond

These long-duration bond ETFs have cratered the most from ... Sep 29, 2022 · That fund, along with the PIMCO 25+ Year Zero Coupon U.S. Treasury ETF ZROZ and the Vanguard Extended Duration Treasury ETF EDV, have all plunged more than 40% from their 52-week peaks, according ... Bond Duration Calculator - Exploring Finance Bond face value is 1000 ; Annual coupon rate is 6% ; Payments are semiannually (1) What is the bond’s Macaulay Duration? (2) What is the bond’s Modified Duration? You can easily calculate the bond duration using the Bond Duration Calculator. Simply enter the following values in the calculator: What’s a bond? | Vanguard Bond duration, like maturity, is measured in years. It's the outcome of a complex calculation that includes the bond's present value, yield, coupon, and other features. It's the best way to assess a bond's sensitivity to interest rate changes—bonds with longer durations are more sensitive.

Duration of a coupon bond. Bond duration - Wikipedia For a standard bond, the Macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero-coupon bond. Modified duration, on the other hand, is a mathematical derivative (rate of change) of price and measures the percentage rate of change of price with respect to yield. What’s a bond? | Vanguard Bond duration, like maturity, is measured in years. It's the outcome of a complex calculation that includes the bond's present value, yield, coupon, and other features. It's the best way to assess a bond's sensitivity to interest rate changes—bonds with longer durations are more sensitive. Bond Duration Calculator - Exploring Finance Bond face value is 1000 ; Annual coupon rate is 6% ; Payments are semiannually (1) What is the bond’s Macaulay Duration? (2) What is the bond’s Modified Duration? You can easily calculate the bond duration using the Bond Duration Calculator. Simply enter the following values in the calculator: These long-duration bond ETFs have cratered the most from ... Sep 29, 2022 · That fund, along with the PIMCO 25+ Year Zero Coupon U.S. Treasury ETF ZROZ and the Vanguard Extended Duration Treasury ETF EDV, have all plunged more than 40% from their 52-week peaks, according ...

What is the duration of a 10-year treasury bond? - Quora

Measures of Price Sensitivity 1

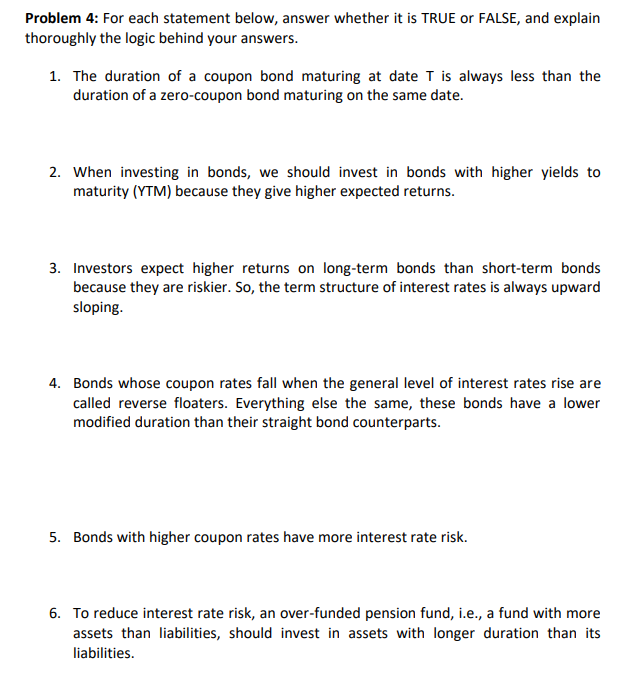

Solved Problem 4: For each statement below, answer whether ...

THE RELATIONSHIP BETWEEN YIELD DURATION AND MATURITY

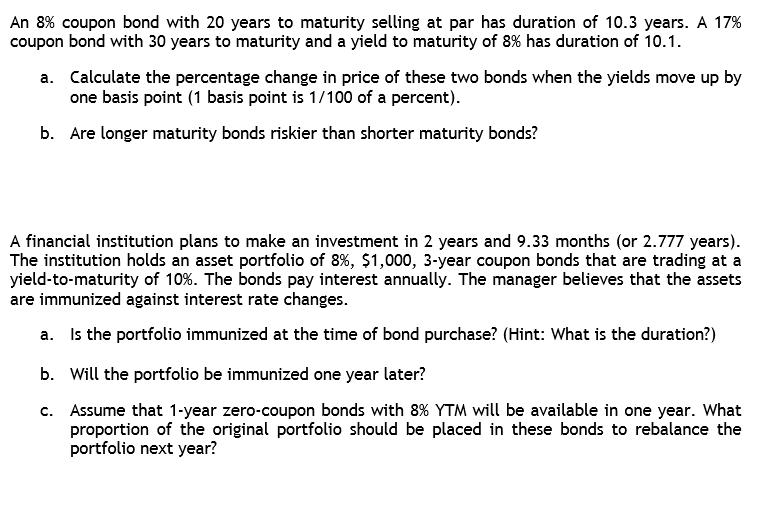

Solved An 8% coupon bond with 20 years to maturity selling ...

Under the Hood: What You Need to Know About Bond Duration and ...

Making sense of duration sensitivity | Fidelity Singapore

Modified Duration - Zero Coupon Bond Modified Duration ...

Duration: Understanding the Relationship Between Bond Prices ...

Bond duration - Wikipedia

What Is Duration of a Bond? - TheStreet Definition - TheStreet

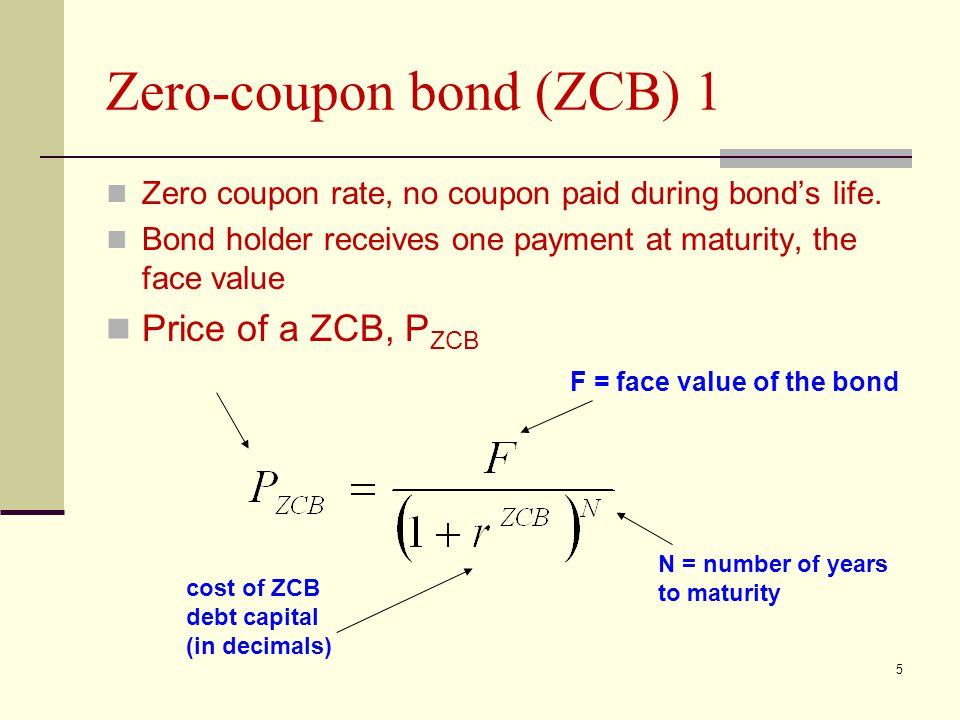

Zero-Coupon Bonds: Characteristics and Examples

SOLUTION: Duration of zero coupon bond - Studypool

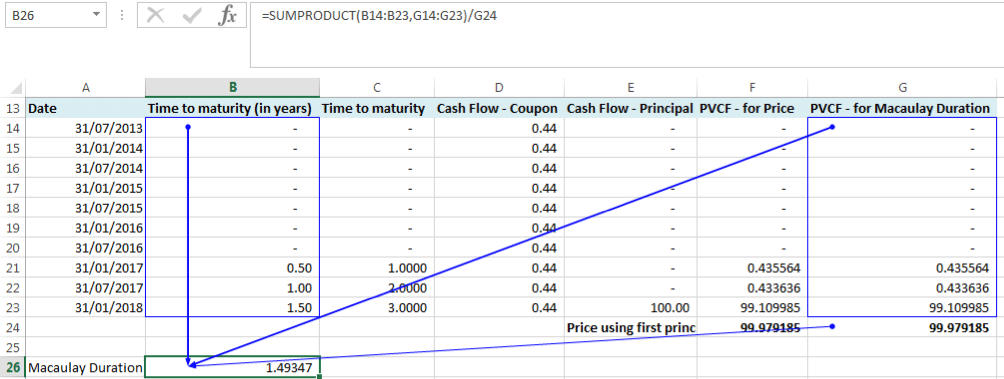

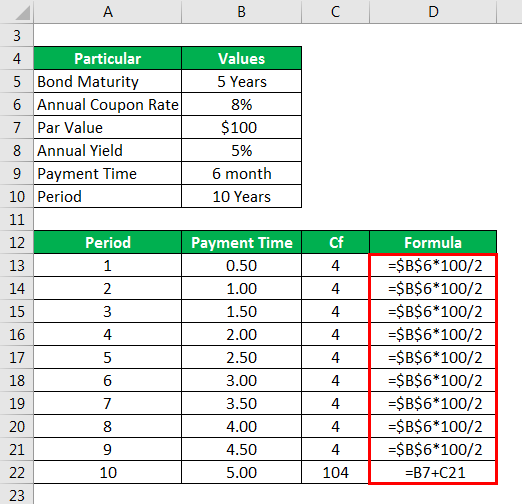

EXCEL Duration Calculation between Coupon Payments ...

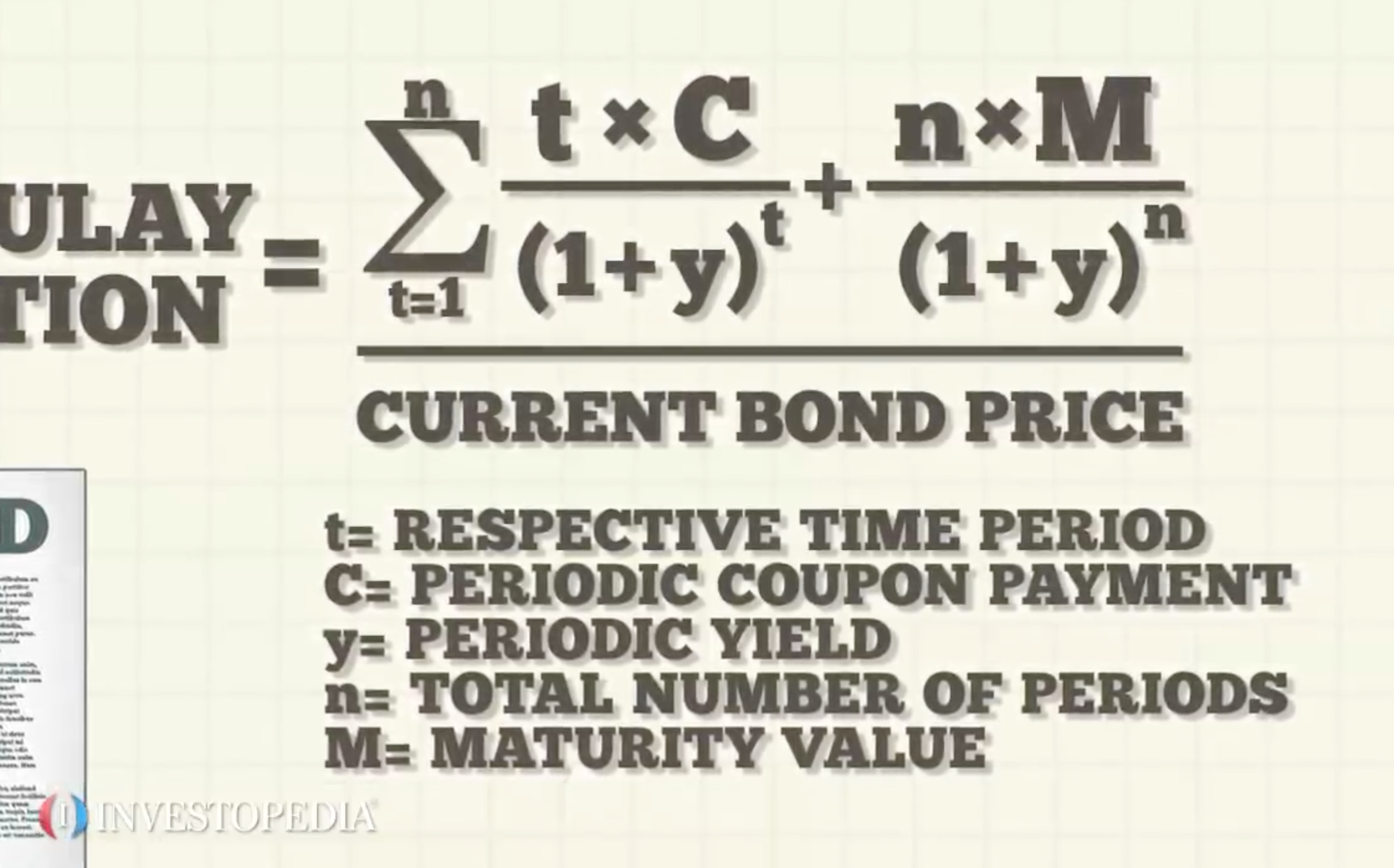

Macaulay Duration

Bond Portfolio Duration and the Flaw of Averages | Morningstar

SOLUTION: Duration of zero coupon bond - Studypool

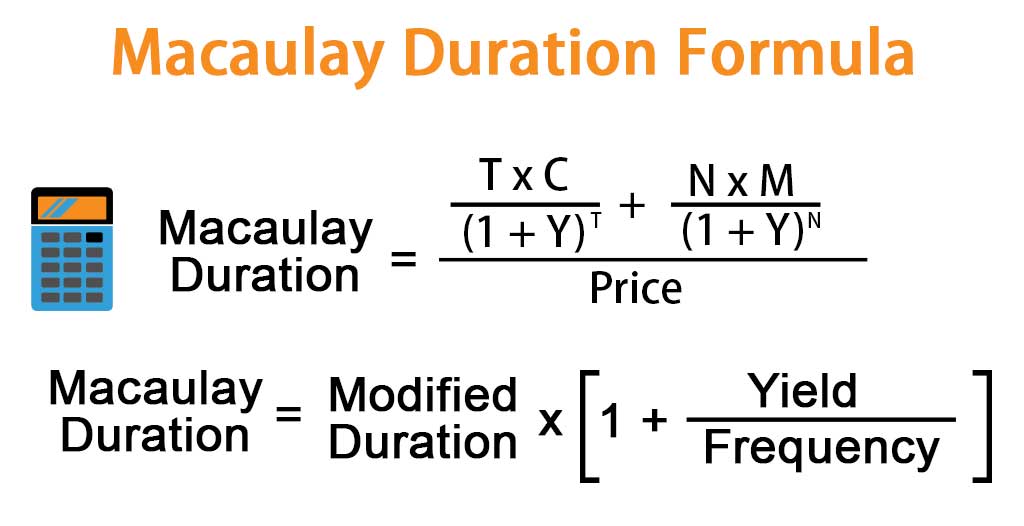

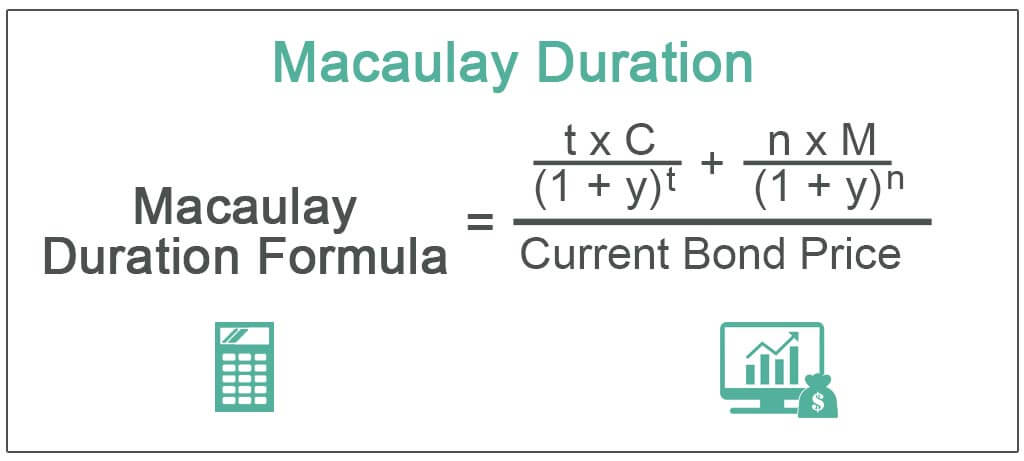

Macaulay Duration Formula | Example with Excel Template

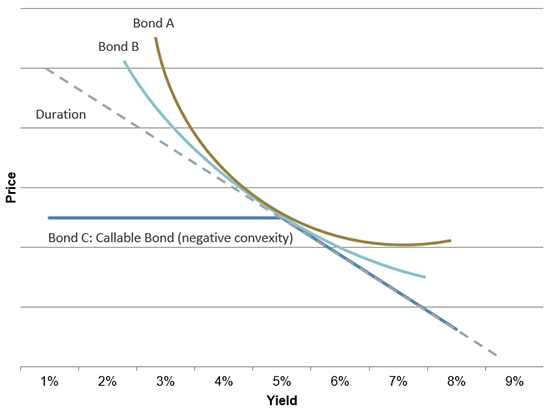

Duration & Convexity - Fixed Income Bond Basics | Raymond James

Zero Coupon Bond - (Definition, Formula, Examples, Calculations)

Macaulay Duration (Definition, Formula) | Calculation with ...

Bond Duration Between Coupon Payment Dates: Financial ...

Duration | Top 3 Types (Macaulay, Modified, Effective Duration)

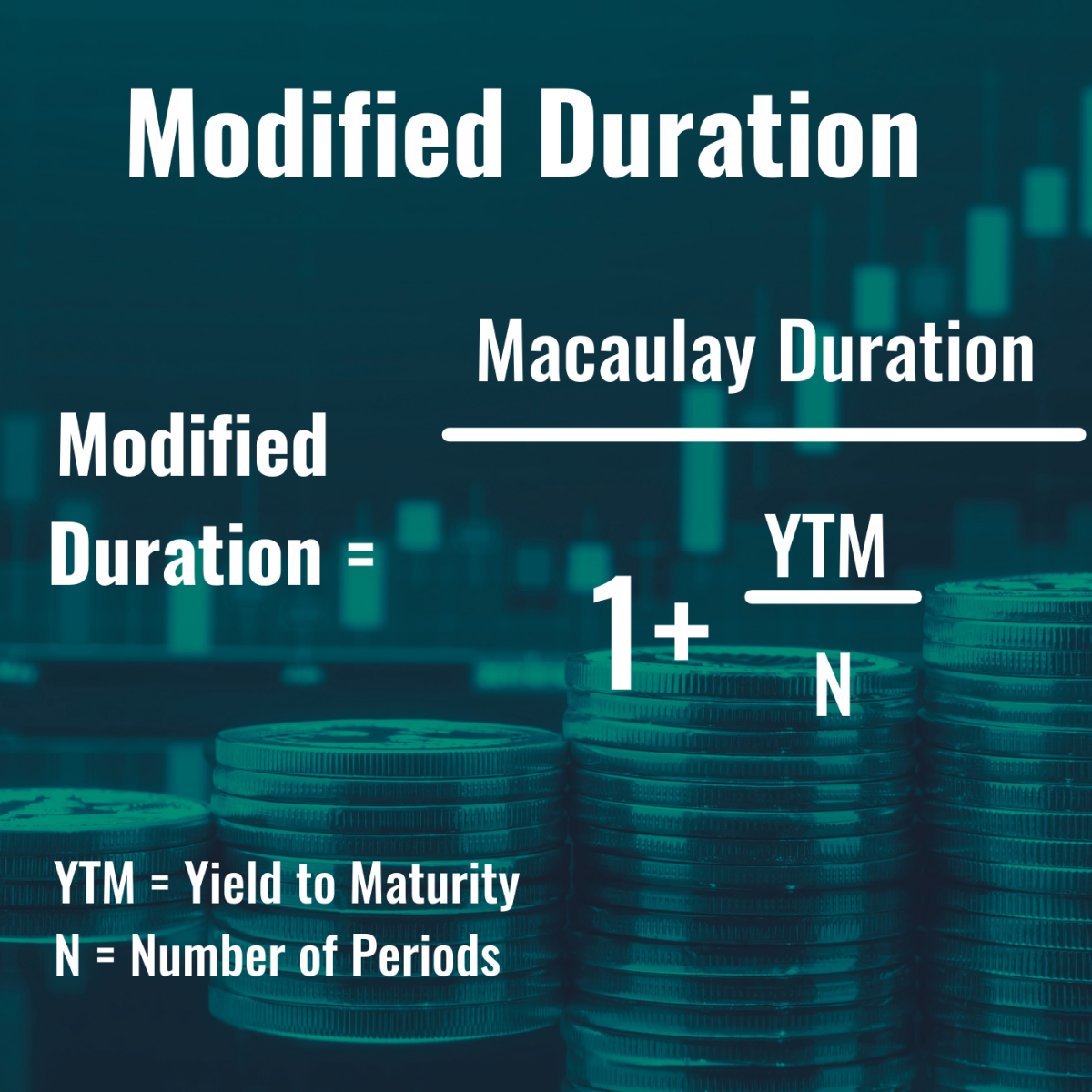

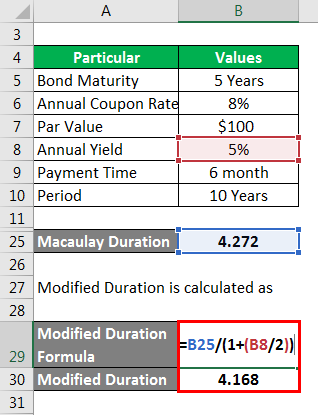

Modified Duration | Explanation, Example with Excel Template

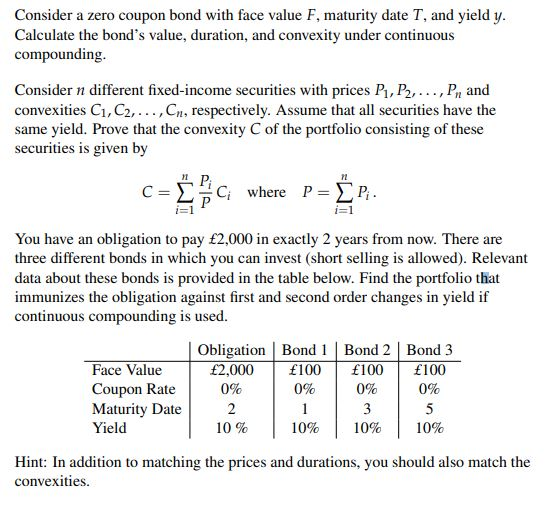

Consider a zero coupon bond with face value F, | Chegg.com

What is the duration of a two-year bond that pays an annual ...

Your Money: How duration of a bond determines its degree of ...

Portfolio Duration and its Limitations | CFA Level 1 ...

Bond Valuation and Risk - ppt video online download

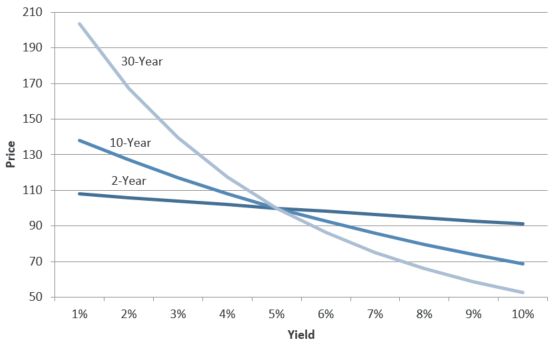

Duration Dv01 Maturity And Coupon A Graphical Analysis - Term ...

Taylor Expansion To measure the price response to a small ...

Premium Bonds 101 | Breckinridge Capital Advisors

Modified Duration | Explanation, Example with Excel Template

:max_bytes(150000):strip_icc()/Duration_final-5225be866f9543a9b4b957620c475cd5.png)

Duration Definition and Its Use in Fixed Income Investing

Macaulay Duration

Duration & Convexity - Fixed Income Bond Basics | Raymond James

Macaulay Duration

Bond Duration Calculator – Macaulay and Modified Duration - DQYDJ

Philip Morris has issued bonds that pay annually with the fo ...

Bond Duration - Understanding Interest Rate Risk

Duration: Understanding the Relationship Between Bond Prices ...

FRM: Dollar duration of zero coupon bond

Post a Comment for "42 duration of a coupon bond"